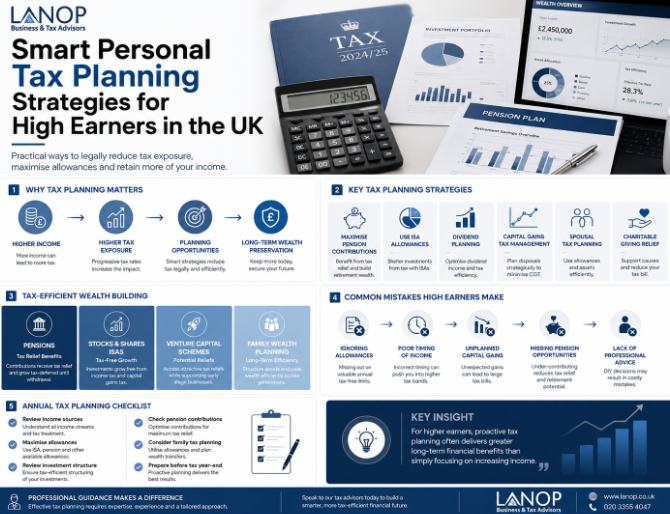

Business

How to Legally Reduce Your Personal Tax Bill Before the HMRC Deadline?

Every April, the same conversation happens in accountancy offices across the UK. A client sits down, reviews their tax position, and asks the question that never gets easier to answer: why did I pay so much?

The honest reply is almost always the same. Not because the tax rates are unfair. Not because the reliefs do not exist. But because the window to use them closed on 5 April, and nobody acted in time.

The UK tax system genuinely rewards people who plan ahead. The reliefs are real, the savings are significant, and none of it requires anything aggressive or complicated. What it does require is action before the deadline, not after. This guide is a practical, deadline-focused action plan built around personal tax planning services that actually move the needle, written for people who still have time to do something about it.

Why Do Most People Overpay Tax Without Realising It?

The problem is rarely the tax rate. It is the timing.

HMRC’s system is structured around a tax year that ends on 5 April. Most reliefs, allowances, and planning opportunities reset at that point and anything unused disappears permanently. The ISA allowance you did not use. The pension contribution headroom you carried from last year. The capital gain you could have managed more efficiently. All of it gone, and none of it recoverable once the deadline passes.

High earners feel this more acutely than most. At £50,000, the High Income Child Benefit Charge begins eroding a benefit many families depend on. At £100,000, the Personal Allowance starts tapering quietly creating an effective 60% tax rate on a band of income that catches professionals completely off guard. Bonus payments and commission structures add another layer of complexity, pushing adjusted net income across thresholds at the worst possible moment in the tax year.

The people who consistently pay less tax than their peers are not in different brackets. They are simply making decisions before the deadline rather than after it.

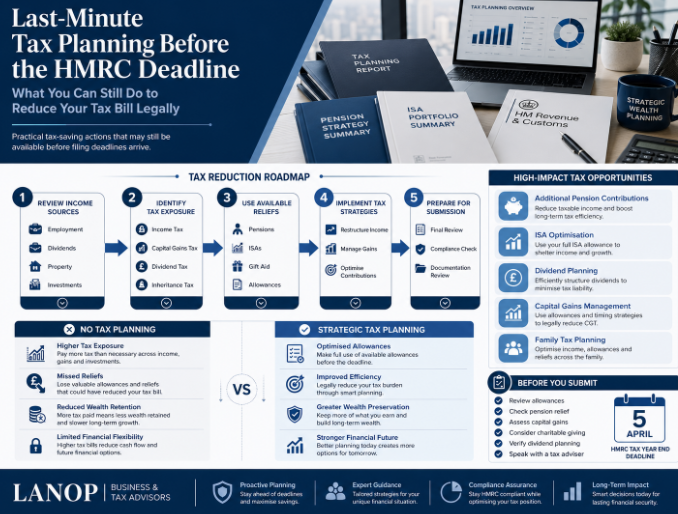

What Does the 5 April Deadline Actually Mean?

The tax year ends on 5 April. That date is not a filing deadline.it is a planning deadline. The distinction matters enormously.

Filing a Self Assessment return happens months later. But the decisions that determine how much tax you owe pension contributions, ISA subscriptions, capital gain realisations, Gift Aid declarations all have to be made before 5 April. By the time most people sit down with their accountant to complete a return, the year is already closed and the numbers are fixed.

What must happen before the deadline:

- Pension contributions for the current tax year must be paid by 5 April. Contributions made on 6 April fall into the following year regardless of intention.

- ISA allowances are use-it-or-lose-it. The £20,000 annual limit resets on 6 April and the previous year’s unused allowance cannot be carried forward.

- Capital gains decisions which assets to dispose of, in which tax year, and in whose name must be crystallised before the year closes.

- Gift Aid declarations reduce adjusted net income for the current year only if the donations are made before 5 April.

Waiting until the tax return is like reviewing the game tape after the final whistle. Informative, but too late to change the score.

The Tax Traps That Hit High Earners Hardest

The £100,000 Income Trap

This is the threshold that generates the most genuine shock among higher earners seeing it properly explained for the first time.

Above £100,000, the Personal Allowance, the £12,570 of income you receive tax-free starts withdrawing at a rate of £1 for every £2 earned above the threshold. By £125,140, it is gone entirely. The consequence is an effective marginal tax rate of 60% on income between those two figures, created not by a higher rate band but by the simultaneous loss of tax-free allowance.

| Income Level | Effective Marginal Rate | Key Impact |

| Up to £50,270 | 20% | Basic rate band |

| £50,271 – £99,999 | 40% | Higher rate band |

| £100,000 – £125,140 | 60% | Personal Allowance taper zone |

| £125,141+ | 45% | Additional rate allowance fully lost |

What makes this particularly painful is that it affects more than take-home pay. Cross £100,000 and free childcare for under-fives disappears. The 30-hour entitlement worth over £5,000 annually for many families vanishes at a single adjusted net income figure. A pay rise of £3,000 can cost a family considerably more than £3,000 in combined tax and lost benefits.

The Bonus and Commission Problem

March bonuses are a structural tax problem that most employers never mention.

A bonus paid in March lands in the current tax year. If it pushes adjusted net income across £100,000, the allowance taper activates for the entire year. If it crosses £50,000 and Child Benefit is in payment, the High Income Charge increases. The employee receives the gross bonus, pays income tax at their marginal rate, and often discovers months later that the net effect was far smaller than expected and that a modest pension contribution at the right moment could have changed the outcome entirely.

RSUs and share awards carry the same risk. When shares vest, the value counts as employment income in that tax year. Without planning around vesting dates and pension contributions, equity compensation routinely generates larger tax bills than necessary.

What You Can Still Do Before 5 April?

Immediate Actions

Check your income position now. Do you know your current adjusted net income? Most people do not until the Self Assessment return forces the calculation. Knowing the number in February or March gives you weeks to act. Knowing it in May means the year has already closed.

Review pension headroom. The annual pension allowance is £60,000. Most people in the £100,000 to £200,000 range use a fraction of it. Even more significantly, unused allowance from the previous three tax years can be carried forward and used in the current year a strategy called pension carry forward that is systematically underused by people who would benefit most from it.

Medium Urgency Actions

ISA contributions do not need to be made in one transaction. Regular monthly contributions throughout the year work just as well. If the full £20,000 allowance has not been used, the remaining months before 5 April still count.

Spouse asset transfers before year-end can rebalance investment income and capital gains exposure between partners. Assets transferred between spouses are treated as no gain, no loss for CGT purposes which means timing a transfer before 5 April can change whose allowances and rates apply to future gains.

Last-Chance Actions

Pension top-ups in March are among the most valuable planning actions available to high earners. A contribution that brings adjusted net income below £100,000 restores the Personal Allowance, saves tax at an effective rate significantly above 40%, and improves the pension pot simultaneously.

Capital gains harvesting deliberately realising gains up to the annual exempt amount is worth doing before the exemption resets. Equally, crystallising losses before 5 April allows them to be set against gains already made in the same year.

The Most Powerful Legal Tax Lever Available(Pensions)

Pension contributions reduce adjusted net income directly. That is the mechanism that makes them so effective for high earners and why structured advice helps optimise pension timing as part of a broader personal tax planning services strategy.

A person earning £115,000 who contributes £15,140 to their pension before 5 April achieves three things simultaneously. Their adjusted net income falls below £100,000. The Personal Allowance is fully restored. And the effective tax relief on that contribution, factoring in the restored allowance, approaches 60% rather than the standard 40%.

Pension carry forward extends this further. If you have not maximised pension contributions in the previous three tax years, that unused allowance carries forward and can be used in addition to the current year’s £60,000 limit. For someone who received a large bonus or equity vesting event, carry forward can absorb a significant income spike in a single year.

Investment Tax Efficiency Before Year-End

ISAs remain one of the simplest and most effective tools available. The £20,000 annual allowance produces tax-free growth and income permanently not just while the money sits in the account, but on every disposal and dividend forever. For high earners whose savings allowance is restricted and whose dividend allowance has been reduced to £500, the ISA wrapper becomes increasingly valuable with each passing year.

Capital gains planning rewards attention to timing. The Bed and ISA strategy selling an investment outside an ISA and repurchasing within it resets the cost basis inside a tax-free wrapper. It uses the annual CGT exempt amount in the process. Done before 5 April, it permanently removes future gains on those assets from the taxable estate.

VCTs and EIS investments offer 30% Income Tax relief on qualifying amounts and are worth considering for high earners with significant tax liabilities, though they carry investment risk and suit a specific profile rather than everyone.

Family Tax Planning: The Most Underused Strategy

Tax planning at household level consistently outperforms individual planning. Two partners with different incomes have options that a single earner simply does not.

Transferring income-producing assets to a lower-earning spouse shifts the tax on dividends, interest, and rental income to a lower rate. If one partner is a basic rate taxpayer and the other pays 40% or above, the same asset generates considerably less tax in one name than the other.

The childcare trap is worth flagging specifically. If adjusted net income crosses £100,000, 30 hours of free childcare disappears often without warning. A pension contribution of a few thousand pounds before 5 April can preserve that entitlement for the following year. The financial value of that action, combining pension tax relief and retained childcare support, routinely exceeds £6,000 for a family with young children.

Year-End Tax Planning Checklist

- Confirm your adjusted net income figure for the current tax year

- Identify which thresholds you are near £50,000, £60,000, £100,000, £125,140

- Review pension contributions made so far this year and check remaining headroom

- Calculate carry forward allowance from the previous three tax years

- Top up ISA to the £20,000 limit if not already maximised

- Review capital gains position harvest gains or losses before 5 April

- Check spouse’s tax position and consider asset transfers before year-end

- Confirm any Gift Aid donations are declared before 5 April

- If receiving a bonus in March, model the pension contribution needed to offset it.

Real-Life Scenarios

Earning £95,000. Minimal threshold risk at current income, but approaching the danger zone. Pension contributions and ISA maximisation keep adjusted net income well clear of £100,000 and build long-term wealth simultaneously.

Earning £110,000. This is the critical planning zone. A pension contribution of £10,000 restores the Personal Allowance and reduces the effective tax rate on that contribution to approximately 60%. Without it, the taper runs its course and the tax bill is significantly higher.

Earning £150,000. Personal Allowance is gone. Pension contributions still reduce the tax rate meaningfully, and carry forward may allow a larger contribution than the current year limit. Bonus and RSU timing become priorities alongside ISA and capital gains management.

Earning £200,000+. The tapered annual allowance applies to pension headroom reduces above £260,000 but does not disappear entirely for most people at this level. Family planning, VCT and EIS consideration, and inheritance tax awareness all come into play alongside the core income tax position.

DIY Tax Planning vs Professional Support

| DIY Approach | Professional Support | |

| Best suited for | Simple salary income, basic ISA usage | Multiple income streams, thresholds, equity |

| Pension carry forward | Often missed | Calculated and maximised |

| Threshold management | Reactive | Proactive planned before deadline |

| Family planning | Usually ignored | Built into household strategy |

| Risk of overpaying | High | Significantly lower |

DIY works for straightforward situations. A single income, no threshold complications, basic savings the HMRC website and a decent accounting package cover most of it. The moment income crosses £100,000, equity vests, rental property comes in, or a bonus creates a threshold problem, the cost of getting it wrong consistently exceeds the cost of professional guidance.

Frequently Asked Questions

What is the HMRC self-assessment deadline?

The online filing and payment deadline is 31 January. However, most tax-saving actions like pension contributions and ISA top-ups must be done by 5 April, the end of the tax year. Miss that date and you lose those allowances for good.

How do pension contributions cut my tax bill?

You get tax relief on pension contributions at your highest rate 20% for basic-rate taxpayers, 40% or 45% for higher earners. Higher-rate taxpayers must claim the extra relief through their self-assessment return or they will miss out.

What allowances am I probably not claiming?

Common ones people miss include the Marriage Allowance, the £1,000 Trading Allowance, the £1,000 Property Allowance, and work-related expense deductions. Check each one there is free money left on the table.

Does an ISA reduce my tax bill?

Not immediately, but any growth, interest, or dividends inside an ISA are permanently tax-free. Using your £20,000 annual ISA allowance before 5 April shelters future gains from HMRC entirely.

How does Gift Aid save me tax?

Higher and additional-rate taxpayers can claim back the difference between their tax rate and the basic rate on charitable donations. A 40% taxpayer donating £100 under Gift Aid can reclaim an extra £25 through their tax return.

Conclusion

Most tax savings are not complicated. They are time-sensitive. High earners lose money every year simply because the right decisions were not made before 5 April the pension contribution, the ISA top-up, the capital gain that could have been timed differently.

The tax system rewards people who act before the deadline, and that is exactly what Lanop Business & Tax Advisors helps you do. From identifying missed allowances to structuring your tax position efficiently, the team ensures no relief is left unclaimed.

If the HMRC deadline is approaching, speaking with Lanop accountants is the most valuable financial conversation you can have right now.

How to Legally Reduce Your Personal Tax Bill Before the HMRC Deadline?

A Complete Guide To Military Court Martial Defense When Everything Feels On The Line

Planning A Successful NDIS Business Launch

4 Ways Data Automation Improves Business Efficiency

Benefits of Installing Timber Sash Windows in Period Properties

Is a Professional Office Relocation Service Worth the Investment? A Cost-Benefit Analysis

Why a Professional Semen Test in Manchester is Your First Step

Trends in Personal Fitness: Embracing Weight Loss Coaching

The Complete Guide to Downloading Pinterest Videos: What You Need to Know

International Tax Planning: A Family Wealth Protection Guide

Who Is Jennifer Rauchet?: All You Need To Know About Pete Hegseth’s Wife

Who Is Mindy Jennings?: All You Need To Know About Ken Jennings Wife

Who Is Klarissa Munz: The Untold Story of Freddie Highmore’s Wife

Who Is Enrica Cenzatti?: The Untold Story of Andrea Bocelli’s Ex-Wife

Who Is Mallory Plotnik?: The Untold Story of Phil Wickham’s Wife

Meet Christina Erika Carandini Lee?: All You Need To Know Christopher Lee’s Daughter

Who Is Allison Butler?: The Life and Influence of Kirk Herbstreit Wife

Who Is Jasmine Gong?: The Life and Legacy of Brad Williams Wife

Can Anything Be Done About the Skyrocketing Prices of Essential Medicines?

Who Is Terrance Michael Murphy?: Everything about Audie Murphy’s Son

How to Legally Reduce Your Personal Tax Bill Before the HMRC Deadline?

A Complete Guide To Military Court Martial Defense When Everything Feels On The Line

Planning A Successful NDIS Business Launch

4 Ways Data Automation Improves Business Efficiency

Benefits of Installing Timber Sash Windows in Period Properties

Is a Professional Office Relocation Service Worth the Investment? A Cost-Benefit Analysis

Why a Professional Semen Test in Manchester is Your First Step

Trends in Personal Fitness: Embracing Weight Loss Coaching

The Complete Guide to Downloading Pinterest Videos: What You Need to Know

International Tax Planning: A Family Wealth Protection Guide

Celebrity2 years ago

Celebrity2 years agoWho Is Jennifer Rauchet?: All You Need To Know About Pete Hegseth’s Wife

- Celebrity2 years ago

Who Is Mindy Jennings?: All You Need To Know About Ken Jennings Wife

- Celebrity2 years ago

Who Is Klarissa Munz: The Untold Story of Freddie Highmore’s Wife

- Celebrity2 years ago

Who Is Enrica Cenzatti?: The Untold Story of Andrea Bocelli’s Ex-Wife